Concentration of AI stocks inside S&P 500 hits dot-com bubble peak

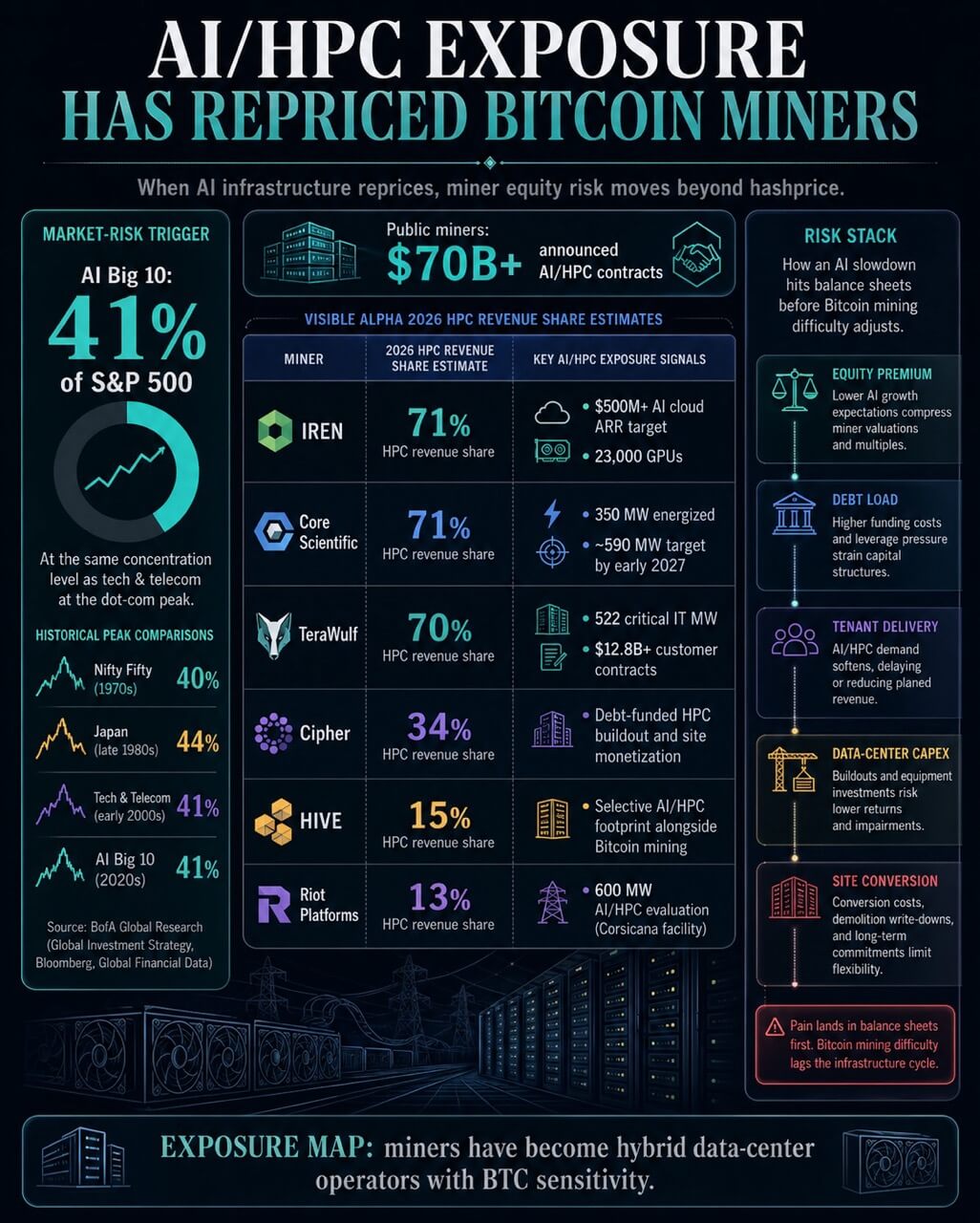

The 10 largest AI stocks now make up about 41% of the S&P 500, according to a BofA Global Research chart circulated online.

That puts the AI basket at the same concentration level that tech and telecom reached around the dot-com peak. The BofA chart put the Nifty Fifty at 40% in the 1970s and Japan at 44% in the late 1980s.

The comparison turns a stock-market concentration warning into a stress test for a corner of crypto that has spent the past year selling investors a new identity.

The market concentration is the stress trigger. Miner disclosures and mining reports supply the exposure map.

Public Bitcoin miners increasingly trade as hybrid infrastructure companies with BTC exposure. Many have signed AI or high-performance computing contracts, raised capital for denser data centers, converted premium power sites, or shifted investor attention toward long-term lease economics.

If the AI infrastructure premium fades, those companies face a different kind of pressure. The risk moves from hashprice alone into debt, contract durability, construction execution, and equity multiples.

At the same time, Bitcoin gets a second-order test. A weaker AI buildout could ease the scramble for power, rack space, interconnections, cooling equipment, and GPUs.

That would hurt miners whose new valuations depend on AI growth, while possibly helping remaining miners if scarce infrastructure becomes easier to secure.

Miners Have Repriced Themselves Around AI

The miner pivot is now measurable in revenue forecasts. A projected revenue mix cited by S&P Global Market Intelligence showed listed miners, including IREN, Riot Platforms, Core Scientific, HIVE, Cipher, and TeraWulf, shifting into AI and HPC workloads.

The projected revenue mix is already large enough to change how these companies are assessed.

Visible Alpha expected HPC to account for 71% of 2026 revenue at IREN and Core Scientific, 70% at TeraWulf, 34% at Cipher, 15% at HIVE, and 13% at Riot.

That spread shows the sector has split into cohorts. Some miners are becoming data-center operators with Bitcoin exposure.

Others are preserving mining as the core business while keeping AI optionality at sites that have power and grid access.

The scale shows up in miner economics. Public miners have announced more than $70 billion in aggregate AI/HPC contracts, according to CoinShares.

The firm also said WULF, Core Scientific, Cipher, and Hut 8 are effectively becoming data-center operators that still mine Bitcoin.

That changes the market link from an AI stock selloff. A falling AI multiple would flow through miner equities because investors have assigned value to the HPC pipeline.

Lower AI demand would also pressure the financing case for projects built around long-duration tenants, higher-density cooling, and premium grid positions.

Mining margins would still depend on BTC price and difficulty, but the equity case would have another variable.

The leverage data points in the same direction. CoinShares said several miners had taken on large debt loads for AI buildouts, including $3.7 billion in convertible notes at IREN, $5.7 billion in total debt at WULF, and $1.7 billion in senior secured notes issued by Cipher.

CryptoSlate has separately tracked how miners have been funding the AI pivot with debt while selling BTC. Put simply, the AI pivot has added a credit cycle to a business that already lived with a Bitcoin cycle.

The table below mixes 2026 revenue estimates, 2025 company disclosures, and contract updates, so each row signals exposure across different time horizons.

MinerAI/HPC exposure signalRepricing pressure pointCore ScientificVisible Alpha projected 71% HPC revenue share in 2026CoreWeave delivery, customer-funded capex, conversion executionTeraWulf522 critical IT MW under long-term leasesFinancing, tenant timelines, and credit-enhanced contract deliveryIRENAI cloud ARR target above $500 million from 23,000 GPUsGPU contract duration, utilization, equipment economicsRiot600 MW Corsicana AI/HPC evaluationValue of using premium power for AI versus miningCipherVisible Alpha projected 34% HPC revenue share in 2026Debt-funded HPC buildout and site monetization

Cipher’s rebrand toward HPC adds another example of the shift. TeraWulf’s Fluidstack expansion shows how miners have paired large power portfolios with AI tenants and credit support.

The Risk Is In The Sites, Contracts, And Capital Stack

Core Scientific is the clearest example of the shift from mining sensitivity to infrastructure execution. In its fourth-quarter 2025 results, the company said it had energized about 350 MW under its CoreWeave contract and remained on track to deliver about 590 MW by early 2027.

It also reported that Q4 colocation revenue rose to $31.3 million from $8.5 million a year earlier, while digital asset self-mining revenue fell to $42.2 million from $79.9 million.

That is the pivot in operating form. Power and buildings once tied mainly to Bitcoin production are being monetized through colocation.

Core Scientific also said $226.2 million of its $279.2 million in fourth-quarter capital expenditures was funded by CoreWeave under existing agreements. That customer funding reduces some capital strain, but it also shows how deeply the buildout depends on an AI tenant’s growth path.

The conversion also introduces accounting complexity. Core Scientific said it was restating prior financial statements after identifying improper capitalization of assets committed to demolition during facility conversion from mining to HPC colocation infrastructure.

The issue was company-specific, but it illustrates a broader point. Moving from mining halls to high-density AI infrastructure goes beyond marketing language.

Core Scientific’s canceled CoreWeave merger agreement shows that AI-linked value already sits inside shareholder decisions.

CoreWeave’s 2025 Form 10-K adds counterparty context, including large contracted power commitments and disclosed risks tied to AI demand.

The miner exposure is, therefore, linked to both site delivery and the financial health of the AI cloud ecosystem.

TeraWulf shows the same shift at a larger contracted scale. In its full-year 2025 results, the company reported long-term data center lease agreements totaling 522 critical IT MW, more than $12.8 billion in long-term credit-enhanced customer contracts, and $6.5 billion in long-term financings.

It said HPC hosting had become its primary growth engine while it continued to operate legacy mining infrastructure opportunistically.

CoinShares reported that WULF mined 262 BTC in Q4 alongside $9.7 million in HPC lease revenue. The same report said WULF’s cost-per-BTC figures were distorted by the company’s transition, including interest, SG&A, and depreciation linked to the new infrastructure base.

That distinction is crucial. Once a miner becomes an AI infrastructure company, per-BTC cost metrics can distort the business unless the balance sheet is separated from the rest of the mining fleet.

Riot’s Corsicana decision shows how AI optionality can alter Bitcoin’s capacity path before a final AI contract even exists. The company’s Corsicana update said it was evaluating AI/HPC uses for about 600 MW of remaining power capacity, halting a previously announced 600 MW Phase II Bitcoin mining expansion, and cutting expected year-end 2025 self-mining capacity from 46.7 EH/s to 38.4 EH/s.

IREN adds a different exposure type. Its October 2025 AI cloud update targeted more than $500 million in annualized AI cloud revenue from 23,000 GPUs by the end of Q1 2026, with 11,000 GPUs contracted for about $225 million of ARR on average two-year terms.

That creates a faster repricing channel than long-term colocation. GPU cloud economics can shift as hardware supply, utilization, and customer budgets change.

Power Scarcity Sets Bitcoin’s Side Of The Trade

The Bitcoin side of the trade is less direct. A weaker AI infrastructure cycle would first pressure AI-exposed miners through equity valuation, funding costs, and contract expectations.

Bitcoin’s network would feel the change through the industrial base that competes for the same power and sites.

The AI-mining link is physical. Bitcoin mining remains the larger aggregate revenue pool in key BTC price scenarios, while AI has become an immediate economic risk to the network’s industrial security base.

AI and mining compete for land, grid interconnections, substations, cooling design, financing, and management attention.

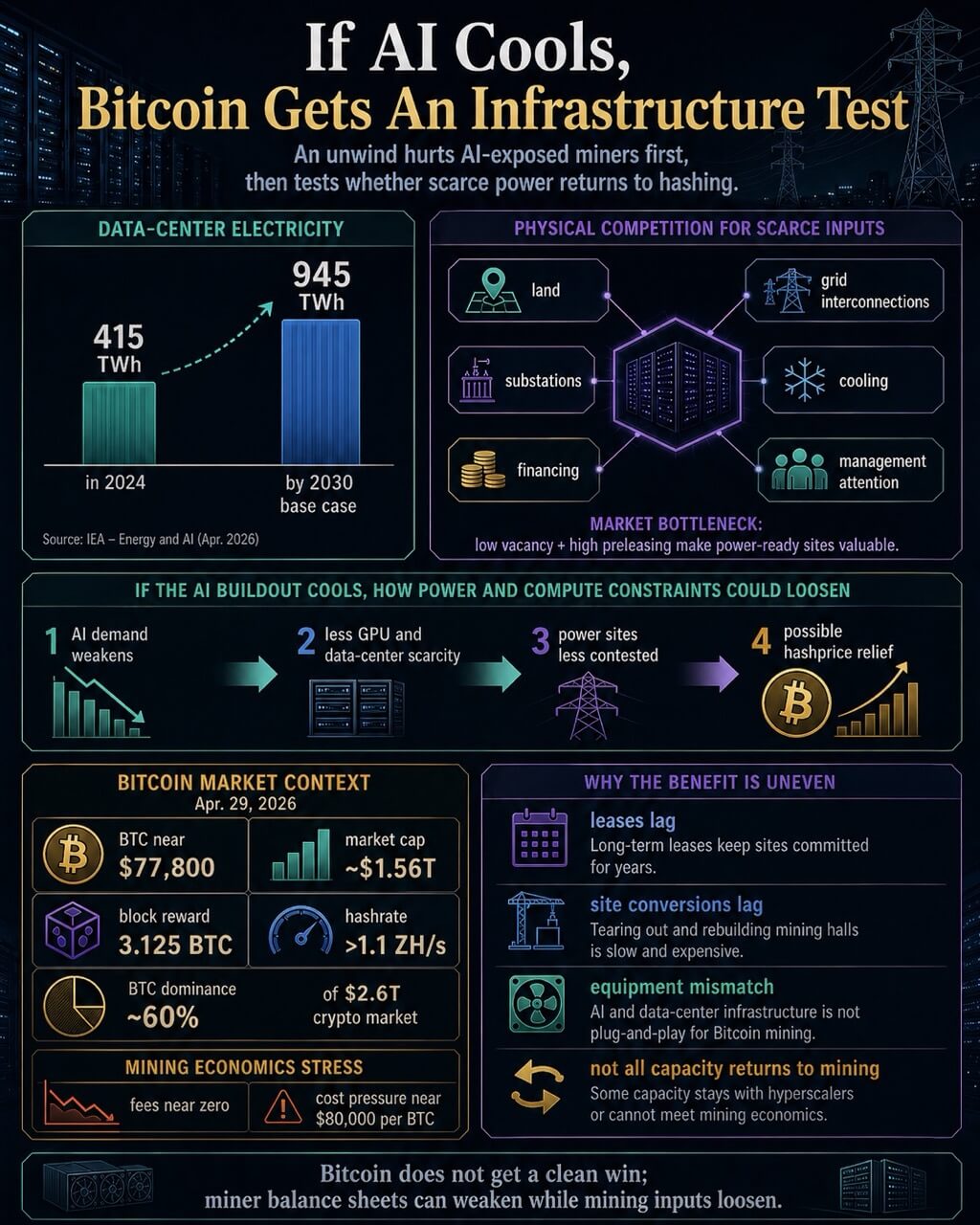

Energy demand from AI explains why the competition is durable. The IEA estimated that data centers consumed about 415 TWh of electricity in 2024 and projected that global data-center consumption would roughly double to 945 TWh by 2030 in its base case.

AI-driven accelerated servers account for a major share of the increase. Data centers can be built faster than power systems can add transmission, substations, and generation, which makes location and grid access valuable.

A North America data-center trends report adds the market bottleneck behind that argument. Low vacancy and high preleasing make power-ready capacity more valuable.

For miners, the scarce asset is often the energized site, with the ASIC fleet only one part of the stack.

As of press time, Bitcoin market data show BTC trading near $76,800, with a market cap of around $1.5 trillion, a current block reward of 3.125 BTC, and a network hashrate above 1.1 ZH/s.

CryptoSlate’s aggregate market page shows Bitcoin’s dominance at around 60% of the $2.6 trillion crypto market. Those figures put miner economics under pressure even before AI competition is considered.

BTC price, fees, difficulty, and energy costs still determine how much security Bitcoin can support.

A cooling AI cycle could ease one part of that pressure. If hyperscaler demand, GPU scarcity, or data-center preleasing weaken, miners that stayed closer to Bitcoin could find power sites and infrastructure less contested.

Difficulty could adjust if capacity exits mining, raising hashprice for remaining operators. That mechanism appears in CryptoSlate’s analysis of miners as AI utilities.

That relief has limits. The fee and cost picture keeps the upside qualified, with fees near zero and cost pressure near $80,000 per BTC.

Difficulty relief alone leaves weak miner economics unresolved. Long-term AI leases, customer-funded buildouts, interconnection agreements, equipment specialization, and site conversion costs also create lag.

An AI unwind would release capacity unevenly, and some of it may remain unusable for mining at attractive returns.

Two Outcomes Depend On AI Demand

The market risk signaled by the AI concentration chart leads to two different outcomes for miners.

In the first, AI demand holds. Public miners with high-quality power campuses keep signing HPC contracts because AI tenants can offer longer revenue visibility than Bitcoin mining.

Premium sites keep drifting toward AI, while mining concentrates around flexible power, demand response, stranded energy, and geographies where interruption is acceptable.

In that scenario, public miner equities become less reliable proxies for BTC because enterprise value comes from leases and data-center execution as much as mined Bitcoin.

In the second, AI infrastructure prices. The miners most exposed to AI growth face pressure through leverage, equity multiples, contract assumptions, and construction pipelines.

Debt raised for data-center buildouts becomes harder to carry if expected AI returns fall. GPU cloud contracts with shorter terms can reset faster.

Long-term colocation leases may offer more protection, although they also lock sites into a path that may take years to reverse.

Bitcoin’s possible benefit sits downstream from that damage. The upside is a loosening of scarce inputs, lower competition for power, and a better hashprice environment for operators still focused on mining.

It is an industrial-security argument, with BTC price sitting outside the direct claim.

That is why the AI concentration chart belongs in a discussion of Bitcoin-miner balance sheets. The chart raises the possibility that the AI trade has become crowded.

The miner data shows which crypto companies have built around that trade. The unresolved test is whether those AI/HPC contracts remain durable enough to justify the shift, or whether the same infrastructure that pulled public miners away from Bitcoin becomes a source of stress.

For Bitcoin, the result would be mixed instead of clean. A repricing could weaken some of the best-capitalized public miners while making energy and data-center inputs less scarce for the miners that remain.

The next signal will come less from AI rhetoric than from financing terms, tenant delivery schedules, new power contracts, and hashprice. Those are the variables that will show whether miners bought a stronger business model or imported a second cycle into Bitcoin’s security base.